There are three major ways to become wealthy in America. Own a business, build wealth through real estate, or invest in the stock market. Today we will focus on becoming wealthy by owning a home. Because it is the American dream anyway and it is the simplest to do and understand of those three.

How much Wealthier can a homeowner be? How about 40 times wealthier?

The Median Net Worth is 40 Times Greater for Homeowners Than for Renters

The best time to buy real estate was years ago. The second-best time is now. This is following the same logic that The best time to plant a tree was 20 years ago. The second best time is now. - Chinese Proverb

But why do I say this?

Let's start with the simple fact that the Net Worth of a Homeowner has been on average211,000higher New worth than a non-homeowner for the last 30 years!

Over 30 years of data can't be wrong!

Here is the impact of Real estate Ownership on NetWorth over the last 30 years.

This chart from 1989-2019 shows the Net worth of House homes vs Renters. Even after the 2007 Real Estate Crash, the New worth of Homeowners stayed almost 200,000 higher than that of renters. It is worth noting alldollar estimates are given in 2019 dollars, this is to remove inflation of the last 30 years.

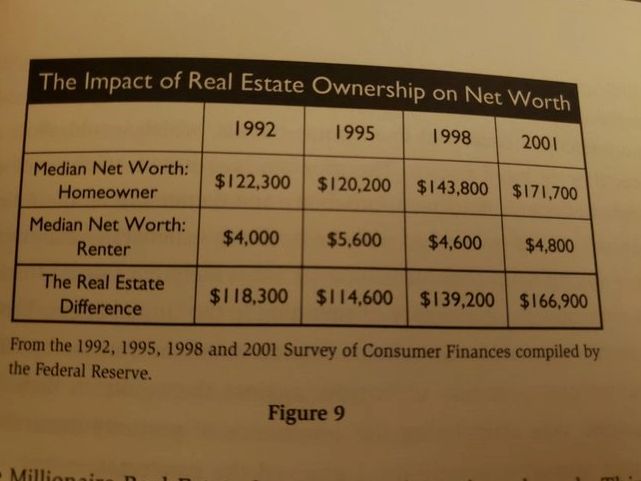

Here are some older data below that shows the Difference in the Worth of Renter vs Homeowners from 1992,1995,1998, and 2001.

What is exactly is Networth?

Net worth is simply the difference between your assets and liabilities, calculated as:

Your Total Assets - your Total Liabilities = your Net Worth

For most people your home is probably your most valuable asset; other key assets include investments, automobiles, collectibles, and jewelry.

The latest Evidence from the Survey of Consumer Finances from 2019 shows the median homeowner has raised to almost over 41 times the household wealth of a renter 255,000 median net worth compared to 6,300 for the renter. That is a difference of 248,700.

You have more options if you have an extra 248,700 worth of dollars.

For families that own a home, the median net housing value (the value of a home minus home-secured debt) rose to about 120,000 in 2019 from about 106,000 in 2016.

When home prices rise, the net worth of households rises too. A tide raises all boats.

Homeowners are wealthier than renters at every income level, and the majority of homeowner wealth comes from housing for every income category except for the very top earners.

Your house is probably your most valuable asset (it may simultaneously be your biggest liability). The more equity you have in your home, the more it will increase your net worth.

Even people with the lowest income have a larger network if they own a home, the median net worth of homeowner households is 102,500, but for renter households, it's only 1,500. In the lowest income category, a full 92% of their net worth is tied to the value of their home.

Begin your search for a new home today. We are local to Katy, Texas.

1. Forced Saving (Saving Made Easy)

Owning a home is how most Americans build wealth. A portion of every housing payment made by a homeowner is applied toward paying down the home loan balance (principal payment), which increases the equity in the home and helps to build a homeowner's net worth. - Carlos Miramontez, V.P mortgage lending at Orange County Credit Union

Paying a mortgage every month and reducing the amount of your principal is like a forced savings plan. Each month you are building up more valuable equity in your home. This equity is essentially part of your net worth, so in a sense, you are preparing for your future without having to think about it too much.

Someday you will have a piece of property that you can sell for profit, rent out, or reap the benefits of living without a monthly mortgage or rent payment.

Learn how much your homeis worth today!

2. A Fixed rated mortgage (Hedging Against Inflation)

The cost of the household stays relatively stable even as your income grows over the years. You pay a smaller percentage of your income to the household. If you rent your cost are likely to go up every year. Were seeing rent prices go up significantly each year, making it difficult for renters to keep up! When you own a home, you will have peace of mind knowing that your monthly mortgage payment will be the same in 5 years as it is now.

The average 30-year fixed-rate mortgage now sits at 2.72%. Near all-time 50 Year lows in fact! There might not be a better time to borrow money for the largest asset you can own.

One of the most significant financial benefits of owning a home is that it protects you during periods of inflation. What does this mean? It means that if you have a fixed-rate mortgage, the price you pay to have a roof over your head can not change no matter what happens to interest rates or the economy. So you know the maximum potential mortgage payment that will be due each month. This can provide peace of mind that is unmeasurable.

3. Saving Money on Taxes. (More Money in Your Pocket)

You can deduct the interest paid. You can also deduct your property taxes which are also likely a large part of your monthly loan payment, and in some cases, you can also deduct your private mortgage insurance. Also when you go to sell you save the capital gain tax from the sale of your main home, you may qualify to exclude up to250,000of that gain from your income, or up to 500,000 of that gain if you file a joint return with your spouse. The only requirement is that you have owned the home for at least two years, or have lived in your home for two of the past five years you've owned it.

4. Building a strong credit history. (Save Money Elsewhere)

As long as you are consistently making your monthly loan payments on time, you are demonstrating to other lenders that you are a good borrower and the risk of you defaulting on a loan is small. This helps to build your credit, which can lessen the cost to borrow future dollars. The lower interest each month saves you more money.

5. Return on Investment. (Appreciation)

You might be thinking well I don't know anything about returns of investments. One of the unique aspects of homeownership as a vehicle for wealth accumulation is that it is one of the few leveraged investments available to households with little wealth are able to use. This allows homeowners with very little equity in their homes to benefit from appreciation in the overall home value. For example, a buyer of a 200,000 home with a 10,000 downpayment will experience a 100 percent return on their investment if home prices rise by a mere 5 percent in the first year of ownership.

Renters don't capture the wealth generated by house price appreciation, nor do they benefit from the equity gains generated by monthly mortgage payments, which become a form of forced savings for homeowners.

6. Non-Financial Returns. (Better Life Satisfaction)

There are many other nonfinancial factors that homeownership brings, that have a positive impact on families. One significant benefit thought to be associated with homeownership is higher life satisfaction and better psychological health. Owners are thought to have higher self-esteem both due to the higher social status associated with homeownership as well as the sense of accomplishment that results from having achieved a significant life goal.

Another important social benefit of homeownership is better life outcomes for children that grow up in owner-occupied homes. Homeownership is thought to benefit children by several mechanisms. Homeownership may enable greater residential stability, which benefits children by providing a stable social and educational environment.

When Buying Real Estate Can Be A Bad Move?

Although owning a home can have many benefits if you're not financially ready it can have devastating effects. As an example, if you stretch your budget or drain your savings to buy a home and then lose it because of a job loss or divorce, this can have a long-term impact on your credit and budget.

We advise that borrowers buy a home well within their budget.

Our biggest advice to first-time owners is not to look at this as a wealth-building move. This is where you are going to live. It's the place where you and your family will build memories, and it's not something you can easily cash in, as the roof over your head is a shelter for your family. That being said, homeownership can lead to wealth-building. The critical element to consider Is location. Where is this home?

All the data, including the most recent data, reinforces that housing is one of the biggest positive drivers of wealth creation. Your Finances Are In Good Shape when you have enough money saved for emergencies as well as for some retirement savings, a low debt-to-income ratio, and a dependable income.

If you want to learn more about how Homeownership can lend to more worth than you ever thought possible reach out to The Gifford Group today.

TheGiffordGroup.net- Opening Doors To New Beginnings

#networth

#homeownership

#renting

#thegiffordgroup

#openingdoorstonewbeginnings

#removethefear

#houstonhomespecialist

#realestate

#houstonrealtor